Last week, Bloomberg published an article titled “Cryptocurrency fans lured by 20% stablecoin yields even after bubble bursts in 2022” [archived link], followed by Matt Levines’ column [archived link] The article was repeated. After speaking with Hannah Miller about this article, I was delighted to read it, but immediately disappointed with the editor's slant. I know that reporters don’t necessarily write their own headlines, which can sometimes cause the tone of an otherwise good story to end up skewed. Regardless, these issues were grossly misrepresented by Bloomberg Cryptocurrency and subsequent reporting by Matt Levine, and I feel the need to clarify them.

The Bloomberg article ends with “the same kind of investment products that led to widespread disaster in the cryptocurrency market in 2022 are proliferating again,” which is wrong. The author is referring to the infamous Terra/Luna protocol, whose UST “stablecoin” went from a nominal value of $18b to almost zero in the spring of 2022. This article covers tokenized Treasury/interest-bearing stablecoins such as Mountain’s USDM or Ondo’s USDY, as well as Ethena’s USDe. None of these systems bear much resemblance to Terra's UST.

As far as I know, no one is trying to rebuild UST today (nor should anyone in their right mind do so). The uncollateralized UST stablecoin, primarily backed by Luna (itself a pseudo-equity derivative of the system), is doomed to fail, and some, myself included, are warning against it. For example, I posted this tweet about Terra on April 21st. On May 8, Terra/UST collapsed.

I also warned about this multiple times on the podcast before the crash, and directly to many colleagues and friends in the industry. I don't say this to pat my chest - I've done that enough - but to make it very clear that I did see Terra coming, that I understood the flaws in the system, and identified the risks before it collapsed. (For a detailed postmortem of Terra/Luna, see my article All Falls Down, co-authored with Allen Farrington.)

At the time, few VCs were willing to talk about Terra because many of them were involved in the industry or didn't want to jeopardize the possibility of investing in the Terra ecosystem if it succeeded. (BTW, this is why few VCs are willing to publicly criticize SBF (like me), since he controls the largest pool of crypto capital at the time). I would point out that Bloomberg is primarily a cheerleader and stenographer for SBF. I don’t think they foresaw Terra’s failure either.

So, as we'll cover here, when Bloomberg suggested I was investing in the next Terra/Luna, they were unfair in several ways:

Most shockingly, this means that all interest-bearing stablecoins have the same risk profile as UST, which is a completely insane outlier

Implying that I lack the ability to assess the risk of interest-bearing stablecoins, I was one of the few voices to accurately identify the Terra debacle before it happened

Implying that I was deceived by the founders, when in fact it was me who had been advocating for the concept of (responsible) interest-bearing stablecoins for months

If this sounds personal, that's because it is. Here are some passages from the Bloomberg article:

The stunning implosion of the TerraUSD stablecoin, and the subsequent bankruptcies of a series of companies that relied on the nearly 20% yields that related projects once offered, exposed just how risky such investments can be.

However, in the world of cryptocurrency, memories can be short. […]

As cryptocurrency players aim to profit from renewed interest in stablecoins, they turn to yield-generating products that some fear could lead to coins that are far less stable than their names suggest. That way. These projects, some of which have interest rates in excess of 20%, have raised concerns that if the mechanisms behind them collapse, holders will be left with a worthless token – which is the case with TerraUSD.

The article goes on to quote myself and Martin Carrica, founder of Mountain Protocol, a seed company led by Castle Island.

They did not mention in the article that UST is an uncollateralized or undercollateralized stablecoin. They mentioned Mountain, Ondo, and Ethena' USDe. Mountain’s USDM and Ondo’s USDY are fully collateralized stablecoins that simply pass on interest in reserves (more on Ethena later). This is exactly how the largest stablecoins work, except the issuer passes most of the interest on to holders rather than keeping it themselves. Obviously, from an end-user perspective, this is an improvement. Would you rather keep all your cash in a checking account that pays 0% interest, or a money market mutual fund that pays 550 basis points? It’s the exact same thing, except issuer liabilities circulate on a public blockchain rather than on a bank ledger.

Stablecoins have not historically done this because stablecoin holders can tolerate the lack of yield when interest rates are low, while the “convenience yield” of on-chain cash instruments is high. Basically, the opportunity cost of forgone gains is affordable because there are many ways to make money with stablecoins and yield mining, among others. However, as crypto rates fell and Treasury rates climbed, capital was sucked out of crypto and back into tradfi (as evidenced by the decline in USDC market cap). This more than anything leads me to believe that stable issuers will be forced to externalize yields on their underlying portfolios.

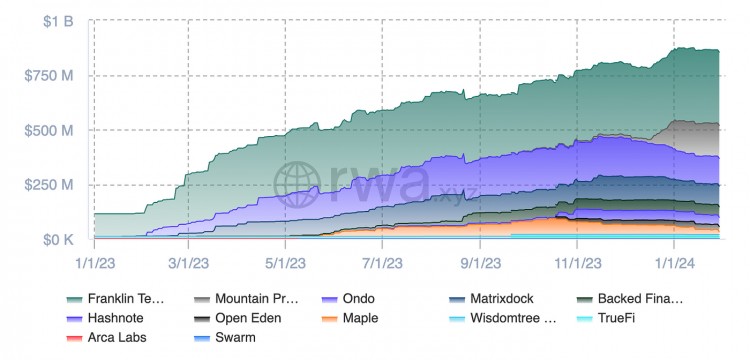

Total tokenized Treasury debt stands at $850 million today, up from almost zero in 2023, although not all tokenized Treasury debt is issued in the form of stablecoins. But these are actually the same type of instrument.

Tokenized Treasury Supply (rwa.xyz)

Tokenized Treasury Supply (rwa.xyz)

These are simple products. Issuers hold Treasury securities and distribute interest to holders. They differ in regulatory approach and compliance/licensing.

It goes without saying that USDM or USDY have nothing in common with UST other than the "stablecoin" title (which I object to anyway, as evidenced by my movement to rename these instruments as cryptocurrencies) . If you ask me, I would say Terra’s UST is not a stablecoin at all, but an unsecured liability of the Terra Foundation. There was a clear gasp when Bloomberg conflated the two. But these similarities are only superficial.

Mountain passes 500 basis points of interest from the underlying Treasury portfolio. UST paid 2,000 basis points of interest based on Do Kwon's financing capacity.

Risks like USDM are the traditional risks faced by all stablecoin issuers: namely smart contract risk, the remote possibility of a liquidity crisis if there is a run or problem on the service provider, and standard regulatory risks. The real “yield” comes from holding short-term Treasury bills. (Incidentally, in Mountain’s case, these assets are held in an FBO trust, which is protected from bankruptcy, which is the optimal structure for a stablecoin). If Bloomberg believes that 3-month Treasuries are as risky as Terra's ability to cash out any 20% interest rate in perpetuity, then they have a very poor view of the U.S. government indeed. There is a possibility that the U.S. government will default. But if it does, we’ll have bigger problems than a tokenized treasury of less than $1 billion.

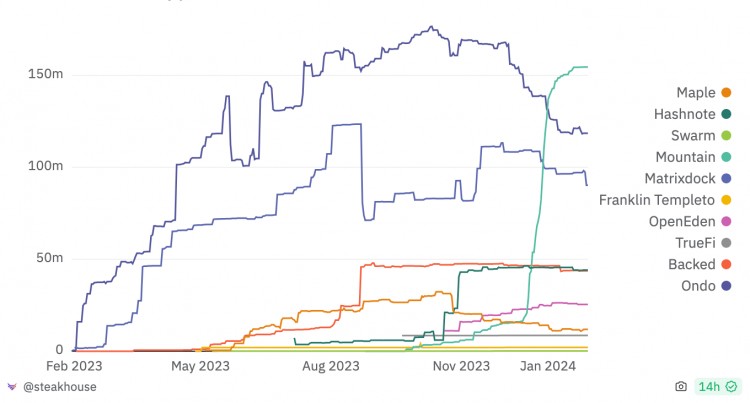

Regarding the other risks, I firmly believe that the Mountain team has processes in place to manage all of these risks, and they have full confidence in me, which is why I led this round in the first place. The system is running. Today, they are the largest interest-bearing stablecoin, having only been around for a few months.

Tokenized Treasury Bills/Interest-Bearing Stablecoins (Steak House)

Tokenized Treasury Bills/Interest-Bearing Stablecoins (Steak House)

In addition to conflating USDM with Terra's UST errors, the article quoted a self-proclaimed expert who at least completely misrepresented Mountain's regulatory strategy. Bloomberg quoted Biglaw partner Michael Selig as saying:

[Stablecoin issuers] attempt to avoid registration and licensing requirements by issuing and redeeming them directly overseas, but allowing stablecoins to flow into the United States through secondary sales.

This is patently wrong. Mountain is a Bermuda company. In fact, they are the first stablecoin to be licensed by the Bermuda Monetary Authority for digital asset operations. They do not do business with US customers (based on the Reg S exception which they wisely comply with). Therefore, there is no concept of "avoiding registration or licensing requirements". Last time I checked, foreign companies that are not headquartered in the United States and do not serve U.S. customers are not subject to the SEC or any other U.S. regulatory agency. Contrary to Selig’s claims, Mountain is by no means “unregulated.”

The BMA is not an unreliable regulator. They are a highly sophisticated top regulator that oversees a third of the global reinsurance market and has issued digital asset licenses to some of the world’s largest crypto companies, including Circle and Coinbase. According to KnowYourCountry, Bermuda ranks 16th globally for anti-money laundering and sanctions compliance, ahead of the United States or the United Kingdom.

Contrary to Selig’s advice, Mountain maintains strict protocols designed to prevent the flow of tokens on the secondary market to U.S. individuals. These include on-chain address monitoring of addresses associated with U.S. persons, off-chain monitoring (including social media, blogs, and news), and a deterrent measure to freeze the assets of holders who violate the terms and conditions. If a major US exchange were to list USDM, Mountain would explain to them that they had violated the terms and conditions and freeze the coins if necessary (although I don't think it would come to that).

What’s more, interest-bearing stablecoins are not particularly important to Americans, for whom access to money market funds or high-yield savings accounts is trivial. By definition, this product is useful for people who do not have direct access to the U.S. financial system.

If Selig or others believe Mountain's registration in Bermuda is fragile, they just need to listen to Bermuda's leadership. As the United States maintains a hostile attitude towards stablecoins, USD stablecoin issuers have gone overseas and have been welcomed by high-quality regulatory agencies such as Bermuda, Singapore or Hong Kong. This demonstrates a blatant failure of American leadership, but that’s another story.

When I went to Bermuda for the Fintech Summit last year, the only crypto project Governor Burt mentioned in his speech was Mountain. Bermuda regulators are proud that they attract the best fintech/crypto talent through their progressive regulatory regime, and they should be. The U.S.’s utterly chaotic treatment of cryptocurrencies means startups and capital will continue to flow abroad, and I’m not at all ashamed of my involvement in this exodus.

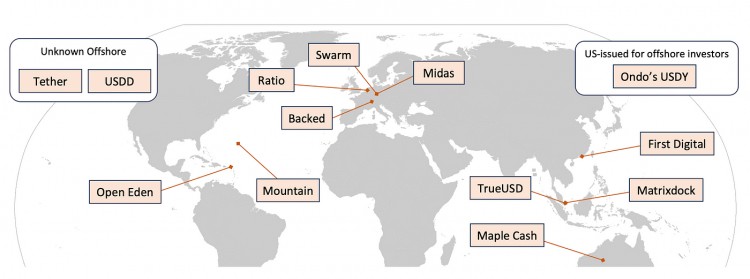

Tokenized Treasury Bills and Interest-Bearing Stablecoins by Domicile

Tokenized Treasury Bills and Interest-Bearing Stablecoins by Domicile

Today, the majority of stablecoins (roughly 75%) are crypto-Eurodollars, that is, they are U.S. dollar stablecoins issued offshore. If Selig believes there are registration requirements with the SEC or other agencies for U.S. dollar stablecoins that do not serve U.S. customers, he should make sure there are laws to do so.

Regarding Ethena, Bloomberg may be referring to them in reference to Terra, but that's still an unfair comparison. Ethena is a synthetic USD token that works by combining a long ETH position with a short futures position. Collateralized ETH pays a yield, and short futures often (but not always) pay a very high interest rate (because there is generally a structurally active demand for long leverage in the cryptocurrency market). The two combine to create a delta-neutral USD position that maintains a positive carry. Granted, this is a different risk than simply tokenizing Treasury bonds, but USDe holders also receive higher yields as a result. And it has little in common with Terra's UST, which offers a completely arbitrary 20% yield without any basis. It's like comparing high-yield credit funds to Madoff's scheme. And, anyway, I've spent several months studying the Ethena system and believe it to be well thought out and very sound - albeit more complex than something like USDM.

Bloomberg columnist Matt Levine also added fuel to the fire. He quoted the part of his colleague's article that quoted me and added the following:

Even outside of stablecoins, there's a general category of financial stories like "someone convinced venture capitalists that reinventing the banking industry was a good idea," and those stories tend to end up in, well, interesting places. (A lot of fintech stories are like this, but FTX’s story is certainly that.) Reinventing banking is a great idea! You can consistently make a lot of money by taking risks that venture capitalists don't notice. “We will take deposits, pay interest, invest the deposits, earn more interest than we pay, maintain the spread, and not be subject to bank capital or prudential regulations” is a great deal for a large part of the time , certainly big enough to raise some venture capital.

This is quite unfair and inappropriate for Levin, who usually performs well. We are not reinventing banking. Mountain is not “unprudentially regulated” (they are regulated as a digital assets business in Bermuda, which has specific expertise and working bodies in digital assets dating back many years). The “venture capitalist” (aka me) is not ignorant of risk.

Mountain founder Martin Carrica didn’t convince me that live stables were a good idea. I've been a believer in this idea for over a year (and have researched many startups in this category). Last fall, I went on a speaking tour laying out the case for interest-bearing stables and gave keynotes at Token2049, Messari Mainnet, and Boston Blockchain Week, where I gave a talk explaining why I thought they were a good idea. I was not deceived in any way and I fully understand the risks here.

I don't think we're reinventing banking as a result. We simply move the database that tracks liabilities from the backend of a bank or asset management company onto the blockchain. There is especially nothing new or unusual about what tokenized Treasury issuers are doing — at least from a risk perspective. The difference is that liabilities circulate freely on a global public ledger, open to virtually anyone in the world. I believe this is a definite good thing and have placed my bets accordingly (trying stuff in Arena, etc.) I believe both Mountain and Ethena are very transparent about the risks and are handling them responsibly - while providing users with Excellent experience.

Aside from the stablecoin name, USDe or USDM bear no resemblance to UST. They are simply not the same thing, and it is completely irresponsible for financial journalists to conflate the two.

It's no exaggeration to say that I've spoken to Bloomberg reporters hundreds of times over the past six years. They asked me to be on TV many times. I consider some of their reporters and analysts to be good friends. That's why I'm particularly disappointed with their recent very strong anti-crypto slant. I expect complex coverage from them, and I know they can do better.

As I discussed during the Messari mainnet demo, it is in the national interest to make clear support for USD stablecoins. Stablecoins export dollars globally, creating huge benefits for large parts of the world’s population struggling with unstable banking systems, weak currencies, and poor property rights. Interest accrual stability is the next evolution and further enhances the value proposition of these instruments. Journalists covering these systems would be better off treating them fairly rather than writing dramatic letters chasing the hobgoblins of the past. We're not asking for preferences or rose-tinted sentiments: just facts, and a fair assessment of the risks and benefits of these systems.

Nothing in this article should be considered investment advice. Mountain's USDM is not available to U.S. individuals. CIV Disclosure. Personal Disclosures.